Category: Trading Career & Structure | Read Time: 10 Minutes

For the developing futures trader, the transition from a simulation environment to a live trading account is the “crossing the Rubicon” moment. It shifts the endeavor from theoretical execution to real-world application. However, once live capital is deployed, a new variable enters the equation that directly impacts the statistical probability of success: Transaction Costs.

For high-volume scalpers or those relying on Order Flow Physics to capture small structural inefficiencies, retail commissions act as a massive friction coefficient. This leads to the most common question among traders graduating from firms like Lucid Trading, The Futures Desk, or Axia Futures:

“How do these firms grant me ‘Member Rates’—exchange fees that are a fraction of retail costs—when I am not an employee and haven’t purchased a $500,000 seat on the exchange?”

To answer this, and to decide whether you should accept a “Live” prop account or take your cash payout to a personal retail broker, we must look at the regulatory machinery beneath the surface.

Part 1: The “Secret” to Member Rates (Regulatory Mechanics)

When you trade a “funded” account, you are effectively trading the firm’s capital. Because the Firm is the Corporate Member of the exchange, the account itself qualifies for low rates. However, the CME and CBOT require a valid legal link between the Firm and the Individual executing the trades.

There are three primary structures firms use to establish this link.

1. The Standard Path: Independent Contractor (Rule 1.2.2)

Used by most modern “Sim-to-Live” funding firms.

CME Rule 1.2.2 allows a Member Firm to grant member rates to independent contractors who trade the firm’s proprietary account.

- The Mechanism: The firm classifies you as a service provider via 1099-MISC. You are not trading your own capital; you are providing the “service” of decision-making.

- The “Pass-Through” Guarantee: Under CME Advisory FPB09-01, firms are prohibited from marking up Exchange Fees. This means the low rate you see is the raw wholesale price passed through to you at cost. The firm cannot hide extra profit in the exchange fee line item.

2. The Equity Partner Path (Class B Membership)

Used by “Deposit-Based” proprietary desks.

Some firms require a significant upfront risk deposit. In exchange, you sign an Operating Agreement to become a Class B Member of the firm’s LLC.

- The Mechanism: Under CME Rule 106.H, equity owners of a Member Firm are entitled to member rates immediately.

- The Benefit: Because you are an owner, you may receive a Schedule K-1, potentially allowing for favorable capital gains tax treatment (60/40 Rule) rather than ordinary income.

3. The “Holdback” Exemption (Rule 106.I/J)

The advanced path for high-net-worth contractors.

This allows an independent contractor to be treated like an owner for tax/fee purposes without buying equity, provided they maintain significant “skin in the game.”

- The Threshold: The trader must maintain a “holdback” of at least $250,000 in accumulated profits.

- The Rules: These funds cannot be deposited; they must be earned from trading. Furthermore, they cannot be held for more than 2 years without the trader converting to a full equity partner. This is why most “Sim-to-Live” traders do not use this path—it requires a quarter-million dollars in retained earnings to activate.

Part 2: The Funded Trader’s Dilemma

Once you understand how the rates are possible, you face a strategic choice. You have passed your evaluation and built up a bankroll (e.g., $15,000 in payouts). Do you:

- Transition to the “Live” Prop Account? (Stay with the firm)

- Go Retail? (Take the cash to AMP/Dorman)

This is a calculation of Tax Efficiency vs. Commission Efficiency.

Option A: The “Live” Prop Firm Account

Best for: High-Frequency Scalpers & High Volume Traders

You enter a Rule 1.2.2 Independent Contractor relationship. You trade the firm’s balance sheet.

The Pros:

- Lowest Possible Fees: You pay raw Member Rates (e.g., ~$1.50 RT for NQ vs ~$4.50 Retail). For a strategy trading 2,000 contracts a month, this saves ~$6,000/month.

- Zero Liability: If the account goes negative, you do not owe the balance. Your risk is capped at your opportunity cost.

The Cons:

- The “Tax Drag” (1099-MISC): Payouts are “Non-Employee Compensation.” You pay Ordinary Income Tax + Self-Employment Tax. You lose the Section 1256 (60/40) tax advantage.

- The 80/20 Regulatory Split: Moving to a live member account often triggers a mandatory 80/20 profit split. This is a compliance necessity to prove the account is “Proprietary” (firm risk) rather than “Customer” (retail). You effectively pay 20% of your profits to access the low commissions.

Option B: The Retail Account (Sole Proprietor)

Best for: Swing Traders & Low-Frequency Day Traders

You wire your payout to an FCM like AMP or Dorman and trade as a Sole Proprietor.

The Pros:

- Section 1256 Tax Advantage: You gain the 60/40 Rule treatment (60% Long Term Cap Gains, 40% Short Term). This is a massive tax efficiency compared to the 1099-MISC structure.

- 100% Profit Retention: No 80/20 split. You keep every dollar you generate.

- Strategic Freedom: No “Daily Loss Limits” or “Trailing Drawdowns” acting as artificial barriers.

The Cons:

- Retail Friction: You pay retail commissions and full professional data fees (unless you qualify for non-pro status).

- Total Risk: Losses come directly from your net worth.

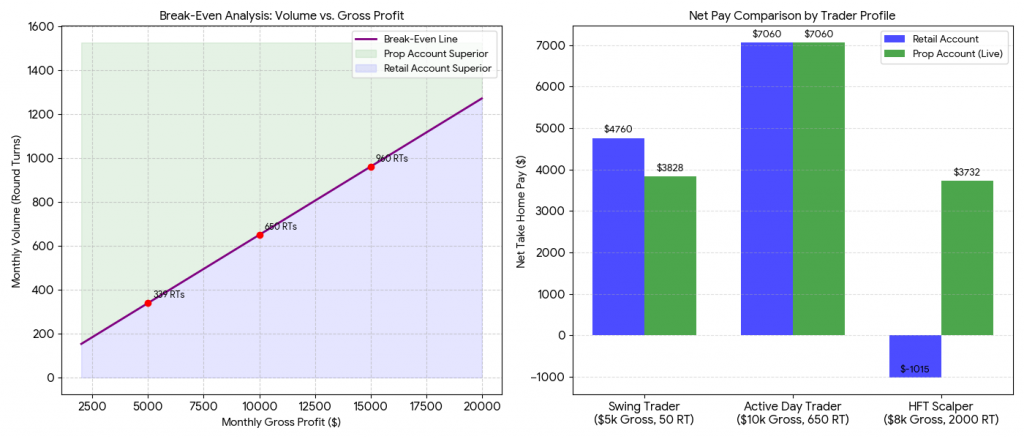

Part 3: The Math (Break-Even Analysis)

Where is the tipping point? We must find the “Indifference Curve”—the exact point where the Commission Savings of the Prop Account outweigh the Cost of the 20% Split and higher taxes.

The graph above illustrates the Break-Even Indifference Curve.

- The Purple Line: Represents the break-even point.

- The Green Zone (Prop Superior): If your trading volume is above the curve, the sheer volume of trades makes the Prop Account mathematically superior. The commission savings are large enough to pay for the 20% split.

- The Blue Zone (Retail Superior): If your volume is below the curve, the Retail Account wins. The commission savings are too small to justify giving up 20% of your profits.

Real-World Scenarios

Let’s plug in real numbers to see how this affects your “Net Take Home Pay.”

Scenario A: The Low-Frequency Swing Trader

Profile: 50 Round Turns/month | Gross Profit: $5,000

- Retail Account (AMP/Dorman):

- Commissions ($4.50 RT): -$225

- Data Fees: -$15

- Profit Split: $0

- Net Take Home: $4,760

- Prop Account (Live Member Rates):

- Commissions ($1.60 RT): -$80

- Data Fees (Professional): -$135

- Profit Split (20%): -$957

- Net Take Home: $3,828

Verdict: Retail Wins. Because volume was low, the commission savings ($145) were negligible. They could not offset the expensive professional data fees and the nearly $1,000 cost of the profit split.

Scenario B: The High-Frequency Scalper

Profile: 2,000 Round Turns/month | Gross Profit: $8,000

- Retail Account (AMP/Dorman):

- Commissions ($4.50 RT): -$9,000

- Data Fees: -$15

- Profit Split: $0

- Net Result: -$1,015 (LOSS)

- Prop Account (Live Member Rates):

- Commissions ($1.60 RT): -$3,200

- Data Fees (Professional): -$135

- Profit Split (20%): -$933

- Net Result: +$3,732 (PROFIT)

Verdict: Prop Wins. For the scalper, commissions are the primary risk factor. The retail rate structure turned a profitable month into a losing one. The Prop Account structure preserved the edge.

Conclusion

The decision to transition to a live Member Rate account is not simply a “promotion”—it is a fundamental change in your business model.

If your edge is built on high expectancy (few trades, large structural rotations), the Retail Route offers superior tax benefits and 100% profit retention.

If your edge is built on high volume/order flow (many trades, small scalps), the Prop Route is essential to survival. The 20% profit split is simply the cost of doing business to access the wholesale fee structure that makes your strategy viable.

Disclaimer: CEED Trading does not provide tax or legal advice. The regulatory structures (CME Rules 106, 1.2.2, FPB09-01) and tax rates discussed are estimates based on US market conditions as of 2025/2026. Traders should consult a qualified CPA or compliance professional.

Getting Real-Time CME Data in Sierra Chart at Non-Professional RatesFutures Trading

Getting Real-Time CME Data in Sierra Chart at Non-Professional RatesFutures Trading From Sim-Funded to Live-Account: The Mechanics of Member Rates and the Retail vs. Prop DilemmaFutures Trading

From Sim-Funded to Live-Account: The Mechanics of Member Rates and the Retail vs. Prop DilemmaFutures Trading- What creates low-volume nodes or why do market makers widen the spread or thin out the order bookFutures Trading

Why Achievable Milestones Are Crucial for Traders with ADHD: A Guide to SuccessFutures Trading

Why Achievable Milestones Are Crucial for Traders with ADHD: A Guide to SuccessFutures Trading 15 Powerful Mindfulness Practices to Boost Trading Focus and Emotional ControlFutures Trading

15 Powerful Mindfulness Practices to Boost Trading Focus and Emotional ControlFutures Trading- How ADHD Traders Can Thrive with Accountability, Milestones, and Mentorship in TradingFutures Trading

- The Main Benefits of Copy Trading Multiple Accounts at Prop Trading FirmsFutures Trading

How Market Makers Use VPIN to Manage Inventory RiskDay Trading Futures Trading

How Market Makers Use VPIN to Manage Inventory RiskDay Trading Futures Trading Main Cause for Anxiety in Traders with ADHD: Ignoring Known Market MechanicsTrading Psychology

Main Cause for Anxiety in Traders with ADHD: Ignoring Known Market MechanicsTrading Psychology- Create your own virtual trading floor assistant using audio alerts in Sierra ChartDay Trading Futures Trading

0 responses on "From Sim-Funded to Live-Account: The Mechanics of Member Rates and the Retail vs. Prop Dilemma"